The financial markets’ focus this week will remain divided between economic fundamentals and the uncertainty around the coronavirus outbreak. On the data front, the week is due to be relatively quiet.

The UK gross domestic product data (GDP) for the final three months of last year will confirm how much output was boosted by December’s election result. The UK’s business sector has shown signs of recovery, prompting the Bank of England (BOE) to keep interest rates on hold last month at 0.75%. However, the BOE downgraded its long-term prospects for the economy by an average growth rate of 1.1% over the next three years. With fourth-quarter (Q4) UK GDP figures being published on Tuesday, investors will gain more insight into the health of the economy.

January’s US consumer price index (CPI) on Thursday is probably the most significant American data release next week. The index will show if the downward trend in prices persists, despite consumers experiencing real earnings strength amidst a tight jobs market. Indeed, inflation remaining below the central bank’s 2.0% target, despite three rate cuts from the US Federal Reserve (Fed) in 2019, is a concern for Chairman Jerome Powell, as he noted in last month’s Fed meeting.

Friday’s US retail sales data for January will reveal if consumer spending started 2020 strongly, after easing in the previous two quarters. In December, growth was 0.3% on a month-on-month basis and consensus is for the same reading again in January.

Also on Friday, Germany reports Q4 GDP numbers. The export-heavy economy struggled significantly in 2019 as trade tensions remained heightened. That said, the economy avoided a technical recession, or output contracting for two consecutive quarters, and Q4 will reveal if news on “phase one” of a US-China trade deal helped alleviate some of the pressures faced.

Mixed earnings season warrants caution

While it’s still early days in Europe, the US earnings season for the final three months of 2019 enters its final stretch with around 60% of companies having unveiled results. So far performance can best be described as “mixed”.

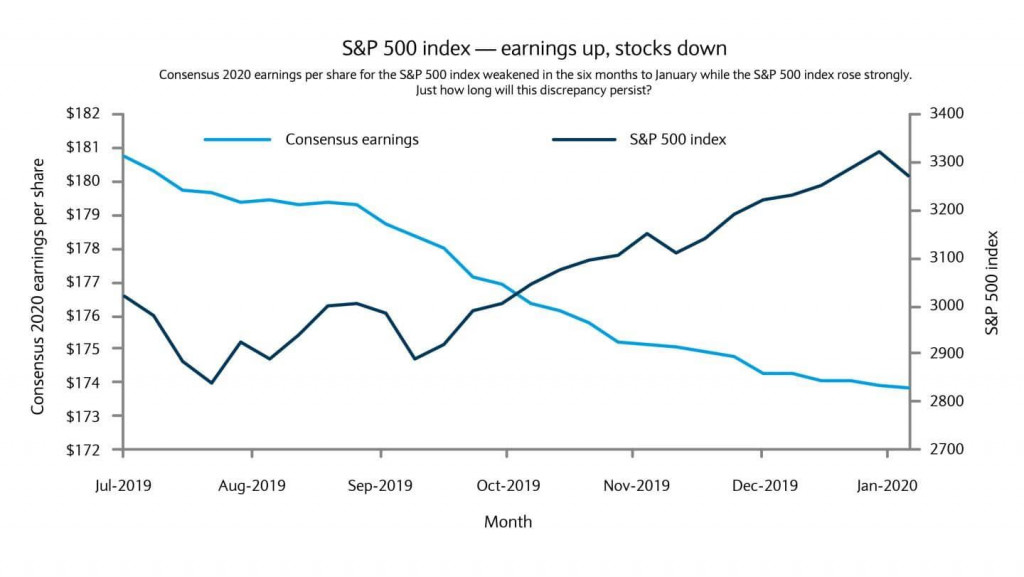

On one hand, as we expected, US companies beat analysts’ expectations once again and are on track to deliver around 2% earnings growth for the fourth quarter. On the other hand, 2020 estimates have bled lower with many reluctant to upgrade guidance in the wake of the coronavirus outbreak in China. Yet, after a short-lived period of consolidation, equity markets are back to posting all-time highs.

The discrepancy between rising share prices and weaker fundamentals (or earnings forecasts for 2020) has pushed valuations significantly above their long-term average (see chart). In our view, such valuation levels leave American equities with very little room for disappointment.

Whether it’s a function of the “known-unknowns”, like this year’s US election, or completely unexpected events as already experienced with the Middle East flare up and the coronavirus, volatility spikes are likely to be more frequent and possibly more pronounced.

While central banks’ liquidity support should prevent significant and long-lasting drawdowns, we believe investors should get ready for a bumpier ride in 2020. First and foremost, this means ensuring proper diversification across asset classes and taking advantage of pullbacks when they present themselves. It also means exploring ways to use higher volatility to enhance, protect and diversify portfolio returns.

For more information contact Barclays Private Bank in Monaco by clicking here or on +377 93 15 35 35